$GMX Fundamentals Part 2

Team, TAM & Comps, Growth, Catalysts, Risks, Price Target

In $GMX Fundamentals Part 1, we covered tokenomics, community, and governance. Today, I’ll start by evaluating team, TAM & Comps, growth, and catalysts.

Then, I’ll share what I think are the main risks, and finally, suggest a price target.

- Sheafson

Topics

Tokenomics (Part 1)

Community & Governance (Part 1)

Team (Part 2)

TAM & Comps (Part 2)

Growth (Part 2)

Catalysts (Part 2)

Risks (Part 2)

Price target (Part 2)

Team

GMX’s core team is anonymous, which has natural pros (narrative) and cons (rug risk). Regardless, they have a 2+ year track record of deft execution and collaboration. To date, there has been no notable management drama or churn.

Here’s a team overview circa Feb ‘22 by @Riley_gmi

While GMX has added devs over time, development is still highly centralized on X, GMX’s pseudonymous leader. X has an impressive track record of prioritizing, coordinating, and shipping fast.

My opinion is that in the early stages of a project where rapid growth and iteration are paramount, the pros of centralization and hierarchy outweigh the cons (google “Sushiswap management” for a case study in the perils of too much decentralization).

Nevertheless, centralizing on X does concentrate risk on one individual, and I'd like to see more explicit planning done to mitigate this key person risk.

In June, X said the team had ~18 months of runway, an optimal amount (too much and too little can both be distorting) for a startup at their stage.

TAM & Comps

Market: A growing decentralized share of a huge derivatives TAM

Perps DEXs can 5x+ volumes (and therefore fees and value) just by getting to parity with today's overall DEX:CEX volume share, not to mention tailwinds of DEX:CEX share growth and overall crypto adoption growth.

We are very early in the growth story of perps DEXs. Here’s why:

As of Q3 2022, DEX trading volumes were 11% of CEX trading volumes

DEXs are volume growing share v. CEXs at 34% YoY (Q3 2022 v. Q3 2021)

Annual overall volume (derivatives + spot) is $54 trillion v. $36 trillion in derivatives volume (70% of total)

Today, 98% of derivatives volume are on CEXs

Top 5 DEX’s futures/perps volume is a meager 2% share

Therefore:

Overall CEX volumes ($54 trillion) are 9x DEX ($5.9 trillion) and derivatives CEX volumes ($35.3 trillion) are 50x DEX ($700 billion)

DEXs are gaining on CEXs at 34% annually

If DEXs share growth v. CEXs goes to zero (unlikely), perps DEX volumes could 5.6x (to $4 trillion) just catching up to current overall DEX:CEX share

If DEXs share growth v. CEXs holds, in 5 years perps DEX volumes could 24x (to $17 trillion) what they are today … and that’s conservatively assuming zero overall volume growth

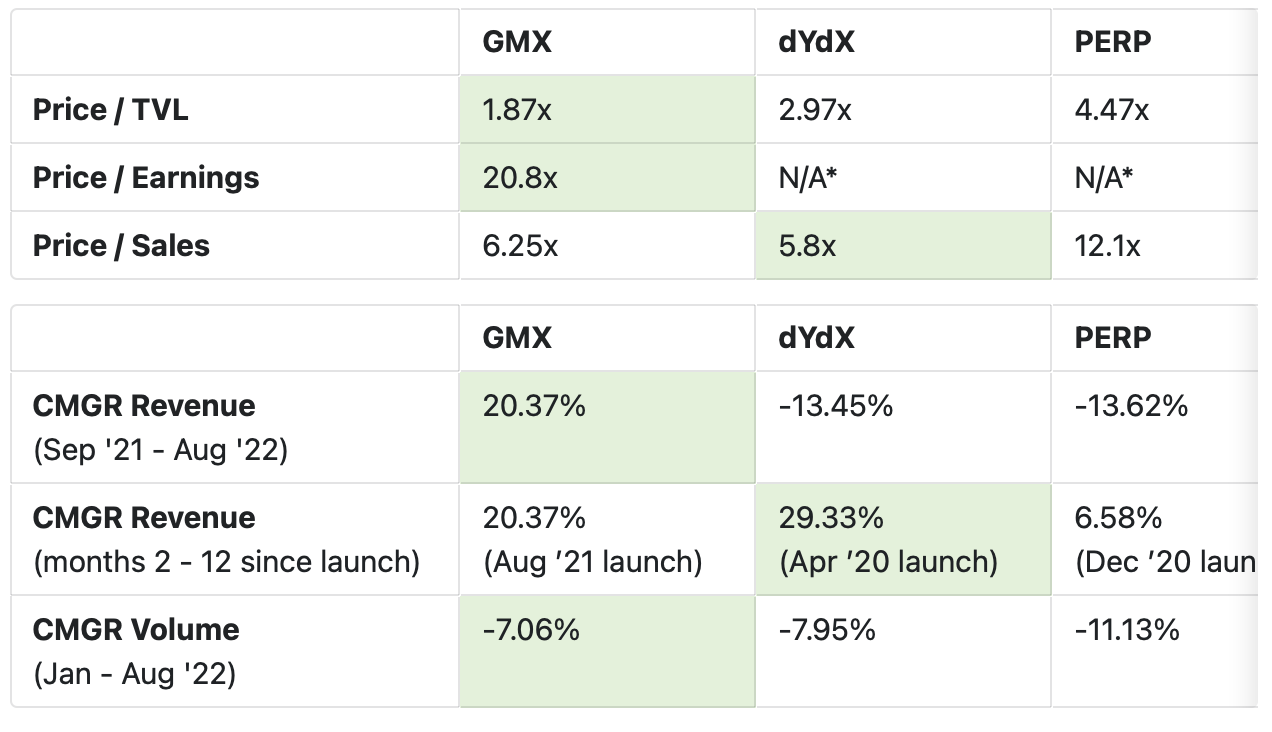

Financials: Strong value v. competitors

On traditional financial multiples, GMX is undervalued v. comps

It’s hard to evaluate most token projects using standard financial multiples because unlike stocks — which get value in standard ways and are subject to standard laws — tokens get value from diverse configurations of properties like direct utility, governance rights, and economic stake — and its rarely apples to apples.

But for projects that look more like traditional businesses and have close narrow category competitors (e.g. GMX) they are a helpful input into reasoning about relative value.

Two call outs:

GMX profits are split between GMX (30%) and GLP (70%). If and when dYdX and PERP begin distributing profits to token holders, we’ll want to incorporate any differences in the share of profits being distributed between the projects

Both dYdX’s and PERP’ teams have said they are working launching a direct value accrual linkage between fees and token holders who stake

Growth

Revenue growth (monetized trading activity)

dYdX grew revenue slightly faster at launch v. comps but GMX has grown faster over the last 12 months (and YTD)

Volume growth (gross trading activity)

Volumes are down everywhere, but GMX volumes are contracting less v. comps

Trading volumes are down across the board, but GMX has a slight edge in average monthly growth between January and August.

User growth up, “engagement” flat

User growth continues to be strong in the broader market downturn, suggesting potential for counter-cyclicality

Since September ’21, total unique users has averaged 15% MoM growth with a sharp spike in June ’22, mainly from traders getting liquidated during the broader crypto deleveraging in that month.

The proxy I’m using for engagement, monthly actions / user, has been flat.

Catalysts

GMX has several major upcoming growth catalysts

Product catalysts

Launch of synthetic tokens, expanding markets (pairs available to trade) significantly for users

X4, a major upgrade that enables

pool creators to customize how their pools behave, like setting a custom fee amount, charging higher fees for selling v. buying, programming fees to decrease over time, among other functions -- unlocking significant programmability and control for pool creators and projects

GMX Swap, an easy-to-integrate “turnkey” swap service for protocols that — if adopted — could significantly ramp adoption and awareness of GMX

liquidity aggregation/routing via other AMMs

among other features (more detail here)

PvP AMM, a novel perps trading approach that replaces the traditional market maker v. trader model with a 3-sided decentralized model. More detail

Potential integrations with other chains and bridges like Synapse Protocol

Marketing and partnership catalysts

Potential FTX listing (discussion, vote)

Cross-arbitrum partnerships e.g. with Plutus (discussion, vote, about Plutus)

Risks

Team risk (key person + anon), regulatory risk, design risk, and competition

Key person risk

The team is highly centralized on X, which is a major key person risk. While I believe the speed benefits of centralization outweigh the cons at this stage of growth, the team ought to do some planning to ensure the project is robust to one failure point. Unless X is multiple people, which of course — since it’s crypto — is possible.

Anonymous team (rug) risk

For traditional companies, good governance looks like an experienced management team held accountable by competent directors, who are in turn elected by shareholders. Bad behavior — which almost always happens behind closed doors — is checked by fiduciary duty, which if violated risks civil and criminal penalties.

In crypto, key people (lead devs, those with access to project funds) are incentivized to behave well by the public nature of blockchains (ex. practically harder to embezzle money), by a desire to preserve valuable and hard-earned reputation, and by fear of public shaming by the community.

All else equal, a doxxed team has more reputation to protect than an anonymous team. But GMX is a decentralized project led by an anonymous team, used by anonymous users, and backed by anonymous tokenholders — which also has its benefits.

Nevertheless, an anonymous team has an elevated “rug risk” that ought to be acknowledged

Design risk

DEXs are recent innovation: Etherdelta launched 2016, Vitalik’s LP-AMM reddit post was 2017, Uniswap V1 launched 2018. As such, the whole category is still iterating to find the most efficient and exploitation-resistant designs — even as it is simultaneously attracting more capital, sophisticated traders, and yield-seeking liquidity providers.

As such, it’s likely that the optimal design choices DEXs will eventually converge on at maturity will be much-improved v. today, GMX included.

One recent (9/18/22) example of this is one savvy trader’s exploitation of GMX’s “zero slippage” oracle-based pricing model to extract $500k in profit from GLP holders by opening AVAX/USD positions on GMX and then pushing prices on external venues in the same direction:

The GMX team responded quickly (again, why I think team centralization is a net positive in early stage projects) to mitigate this specific issue by adding position size caps for low liquidity markets. I’ll be looking to the team to announce further optimizations around this problem, ideally in advance of their much ballyhooed upcoming launch of synthetic assets, which depend on oracle-based pricing.

The team’s ability to iterate rapidly on both product and core mechanism design while scaling volume and users (including increasingly sophisticated ones) is crucial to the success of GMX.

Macro risk

We’re in a highly unfavorable macroeconomic environment for long-duration assets, and absent positive macro catalysts (mainly meaningful progress on inflation), the macro overhang remains a downside price risk for all crypto in USD terms.

Regulatory risk

This is a risk for all decentralized exchanges as a category, not just GMX. We will likely get more concrete guidance on whether and how regulators will treat DEXs over the next 12 months.

Smart contract risk

While allocating treasury budget to bug bounties is a good step, smart contract risk is germane to all blockchain-based products, but particularly complex financial products like GMX that require highly technical code and write permissions on your funds. More transparency on audit process would help mitigate this

Platform risk

While the team has said they plan to expand to other chains, GMX currently lives on Avalanche and Arbitrum. Therefore it inherits platform risk (both technical and social) from these two chains.

Competition

GMX faces competition for crypto perps users from scaled centralized exchanges like FTX, Binance, and ByBit as well as from decentralized exchanges like @dYdX and @Perpetual Protocol.

Developing open software in crypto (especially in its biggest current category) — also naturally invites competition from below. Notable emerging competitors include @GainsNetwork_io and @mycelium_xyz, both of which as of September are doing around 1/10th of the volume of GMX.

Both winning new users from scaled competitors and retaining current users from churning to new challengers require GMX to keep listening to and shipping rapidly for its users.

Illiquidity risk

The same dynamics that incentivize token holders to lock up large amounts of the circulating token supply also leads to low liquidity, which could mean high slippage when entering / exiting a position and higher price volatility.

Price target

Cancelling out GMX’s qualitative advantages and risks relative to peers, relative to comps GMX appears fairly valued at a range between Ξ0.051 and Ξ0.07 (1.89x to 2.5x its current price of Ξ0.027 at time of writing)

Broad category comps

Splitting the difference between BNB’s (conservative given it’s based on a historically bad Q2) and FTT’s P/E multiples, we get something like 41x, which would price GMX at Ξ0.053

Narrow category comps

Splitting the difference on Price / TVL with dYdX and PERP would price GMX at Ξ0.054. Splitting the difference on Price / Sales with dYdX and PERP would price GMX at Ξ0.039. But since it’s growing faster, I think it’s fair to add a 30% growth premium, giving us Ξ0.07 on P/TVL and Ξ0.051 on P/S.

Great write up. Detailed, and including real risks. Pros and cons clearly stated. Kudos.