Introduction

For years, perpetual futures (perps) — crypto’s most popular derivative instrument — were only available on centralized exchanges (CEXs) like Bitmex, with decentralized exchanges (DEXs) largely limited to spot swaps.

But with recent improvements in infrastructure and leveraged trading design, a new crop of DEXs are enabling users to trade perps with UX approaching that of a leading CEX while retaining the benefits of a DEX (trustless, permissionless, private, transparent).

GMX is one of the fastest-growing of these perps DEXs. The platform and use cases have been well-introduced (Bankless, @Riley_gmi, GMX gitbook) so instead I'm going to focus on evaluating the GMX token on fundamentals1, which in my opinion is an increasingly viable valuation approach deploy given the increasing existence of actual revenue and users in blockchain / crypto / Web3.2

Disclosure + Spoiler: I have been long since July and believe GMX is fairly valued in a range between 0.051Eth and 0.07Eth, 1.89x to 2.5x its current Eth price.

Below is an outline of the analysis I plan to cover over the next few posts. I hope you find them useful in sparking new ideas or refining your own framework on valuing public crypto tokens.

Topics

Tokenomics (Part 1)

Community & Governance (Part 1)

Team (Part 2)

TAM & Comps (Part 2)

Growth (Part 2)

Catalysts (Part 2)

Risks (Part 2)

Price target (Part 2)

It’s still early days to identify reliable patterns in growth and monetization in crypto, and therefore also early for fundamental analysis as a useful tool. I welcome your feedback and hope to refine my thinking with you as we all grow up with this category.

- Sheafson

Today I will focus on the first two topics above.

Tokenomics

Economic value accrual from “real dividends”

How economic value accrual happens:

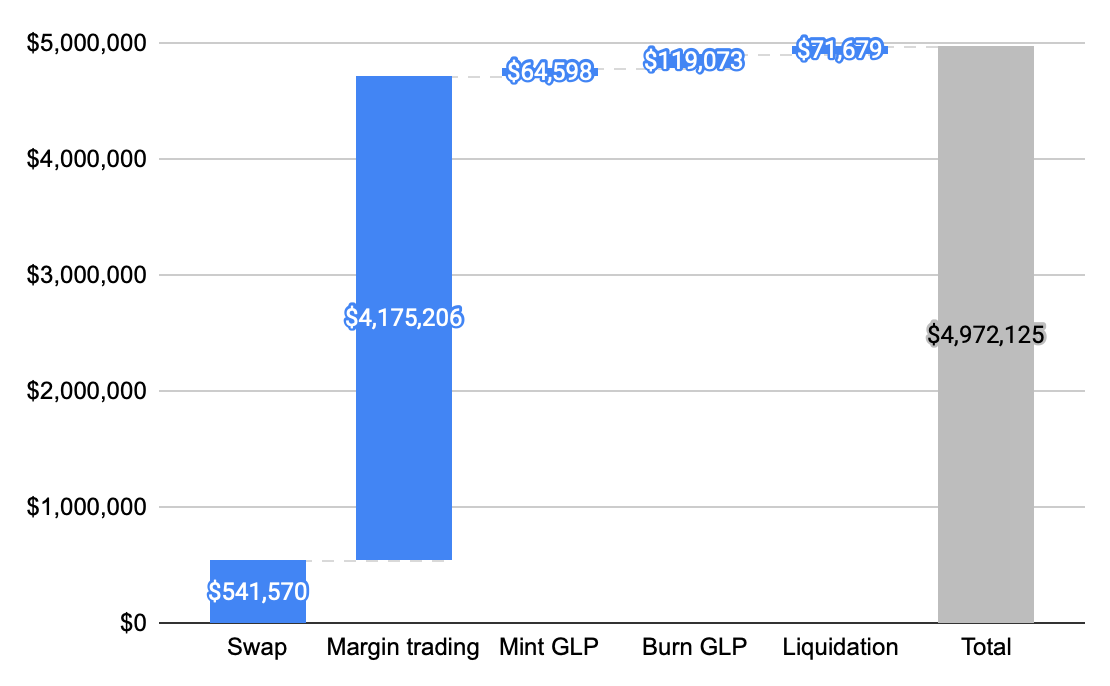

1. Users pay fees to the platform from doing swaps, margin trades, minting/burning GLP, and getting liquidated3

2. 30% of net fees are distributed to staked GMX token holders4

3. Fees are paid out in liquid ether + locked esGMX (for Arbitrum stakers) or in liquid AVAX + locked esGMX (for Avalanche stakers)5

Anti-sell pressure: exogenous rewards, compounding, and sinks

GMX avoids 2020-2021 vintage DEX bootstrapping tactics like bribing users with native tokens, most of which automatically ends up as continuous sell pressure on the token.

Instead, GMX uses mechanisms that encourage locking circulating + newly emitted supply:

Holders who stake their tokens get a proportional share of platform fees in the form of Ether/Avax + esGMX rewards (per above)

Holders who choose to stake their esGMX rewards (instead of vest) proportionally increase their share of platform fees, effectively compounding their earnings

The prospect of compounding also incentivizes holders to convert their liquid Ether/Avax rewards into more GMX

Holders who choose to vest esGMX rewards (instead of stake) must lock the same amount of GMX they originally used to generate those rewards throughout the 365 day linear vesting period (though they’re free to withdraw vested GMX + principal at any time)

Token supply: fair(ish) launch, distributed allocation, incentivized for long term growth

A healthy supply distribution optimized for long term stakeholders

GMX’s only private capital raised is from the initial fundraises of its merged predecessors Gambit6 and XVIX, which were both fair(ish)ly launched — “ish” because Gambit’s raise had a 5% team allocation and I couldn’t verify if there were anti-Sybil measures (the lack of which could have enabled an insider or whale to bypass the per wallet cap by using multiple wallets)

There have been no additional private funding rounds for GMX: no VC round, no private whale round (I couldn't verify whether team sold any tokens or rights to tokens OTC)

Con: less capital to fuel fast growth

Pros: holders and team are much more long term aligned; no low basis VC / whale / insider / partner / [insert shitcoin waterfall participant] overhang waiting to be dumped on retail

GMX tokeholders are by and large independent users, liquidity providers, investors, and partners. The GMX team has allocated themselves less than 2% (low, even if you assume an additional 2-9% from the GMT presale) unlocking (vesting) linearly over 2 years. The remaining supply is protocol controlled and reserved for marketing, liquidity, and security.7

Circulating supply: mostly issued

Low remaining issuance (inflation / dilution) + low likelihood of large blocks of remaining issuance immediately getting sold into the market

As of August 2022, ~75% of the supply has already been issued, with 97% of the remaining issuance protocol-controlled and earmarked for activities that benefit GMX users and token holders.

Community & Governance

An engaged community

GMX’s community is active and productive. Spend time in GMX’s community venues and you’ll see discussions about product and growth outweigh speculation.

Social engagement snapshot (August 16, 2022 at 11:29:08 PM EDT):

GMX Discord online / total: 0.25 (dYdX: 0.06, PERP: 0.19)

GMX Telegram online / total: 0.07 (dYdX: N/A, PERP: 0.06)

Community-grown activities include marketing partnerships, product features, and useful ecosystem projects.

One well-executed community-grown project by @xm92boi is GMX Blueberry Club (GBC), an NFT collection that raised over $1.5m in its December '21 mint. Since then, GBC has collected over $1.23m in esGMX rewards in its community-governed treasury. GBC has an ambitious roadmap focused on delivering value to NFT holders and the larger GMX community (Ex. NFT holders who also stake GMX receive additional esGMX rewards)

A community that generates ideas and leadership that listens

Spend time on GMX’s governance forum, and you’ll notice team leads refining community-originated proposals, and integrating community input on team-originated proposals.

Example: community-originated proposal

Example: team-originated proposal

More decentralized power v. peers

Using snapshot.org voter distribution as a barometer, GMX's voter base is more decentralized than Perpetual Protocol and dYdX.

Last snapshot.org proposals of GMX v. PERP v. dYdX (as of 8/16/22):

GMX's had ~17% participation. The top wallet controlled 13% of the vote

PERP’s had ~8% participation. The top wallet controlled 70% of vote

dYdX’s had ~20% participation. The top wallet controlled 48% of the vote

Next up: Team and Valuation…

Not financial advice. Do your own research.

I wrote this in fits and bursts over the last few weeks, so some of the numbers may be out of date. Also I tried to validate data from multiple independent sources (on-chain explorers, community dashboards, public dashboards, proprietary analytics platforms), but there could be errors. If you notice anything wrong, let me know. —> https://twitter.com/0xSheafson

July fees (Arbi + Avax):

Here’s how fees are distributed to GMX holders, using the week ending in August 13 as an example: $1,838,692 (gross fees) - user rebates (.8%) - affiliate marketing bounties (.8%) - protocol controlled treasury top up (6%) = $1,695,321.9 in net fees - GLP distribution (70%) = $508,596.57 distributed pro rata to staked GMX holders

The protocol currently targets (subject to governance) ~20-25% APY to GMX stakers, paid out in two assets:

(1) liquid Ether/Avax (2) illiquid esGMX

What’s esGMX?

EsGMX (escrowed GMX) earned is unvested GMX that holders can decide to:

(1) Convert to liquid GMX, subject to a 1 year continuous linear vest (2) Add to staked GMX, where it earns fees like regular GMX except but can’t be withdrawn unless converted via (1)

GMT Launch detail (Source: Link + Discord post by y4cards)